Page 10 - ITAtube Journal 2 2022

P. 10

Market information

Figure 1: congestion of transport ships off the coast of China Source: marinetraffic.com

the Corona-related lockdowns in China

are lifted, it will take months for these supply bottlenecks to return to normal.

In the wake of these logistics bottlenecks, the cost of a standard 40-foot container

on the major east-west routes has risen from less than US$2,000 to more than US$10,000 since the beginning of 2020. Chinese pipe producers are currently par- ticularly affected by this, as they can hardly transport their goods to their international destination markets.

As far as possible, the industry is trying

to compensate for these bottlenecks with alternative sources of supply. However,

it has become apparent that in the past decade’s dependencies have arisen here, not only in energy supply but also in raw materials, which can hardly be alleviated

in the short term. This bottleneck is cur- rently leading to a boom in demand on

the local markets, which in turn is causing prices to rise. In this context, the current trend towards decoupling, i.e. becoming independent of singular sources of supply or supplier countries, poses great chal- lenges for our industry. Anyway, it is to be hoped that post the current conflicts on the eastern borders of Europe, trade relations with neighbouring European countries will return to normal while avoiding unilateral dependencies.

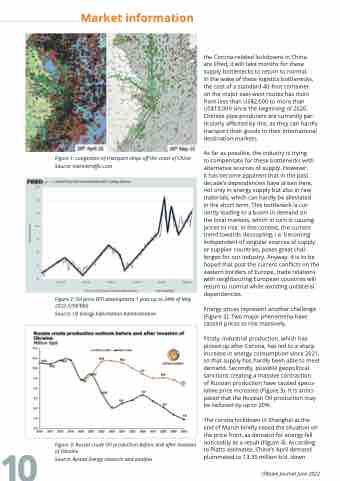

Energy prices represent another challenge (Figure 2). Two major phenomena have caused prices to rise massively.

Firstly, industrial production, which has picked up after Corona, has led to a sharp increase in energy consumption since 2021, so that supply has hardly been able to meet demand. Secondly, possible geopolitical sanctions creating a massive contraction

of Russian production have caused specu- lative price increases (Figure 3). It is antici- pated that the Russian Oil production may be reduced by up to 20%.

The corona lockdown in Shanghai at the end of March briefly eased the situation on the price front, as demand for energy fell noticeably as a result (Figure 4). According to Platts estimates, China’s April demand plummeted to 13.35 million b/d, down

Figure 2: Oil price WTI development 1 year up to 24th of May 2022 (US$/Bbl)

Source: US Energy Information Administration

10

Figure 3: Russia crude Oil production before and after Invasion of Ukraine

Source: Rystad Energy research and analysis

ITAtube Journal June 2022